Economic indicators suggest a period of significant instability. Oil prices remain above $111 per barrel as the strait of Hormuz—a corridor for a fifth of the world’s oil—remains a geopolitical flashpoint. In the industrial sector, manufacturers are grappling with some of the sharpest cost increases seen in over three decades. Despite these pressures, the UK residential property market has remained resilient.

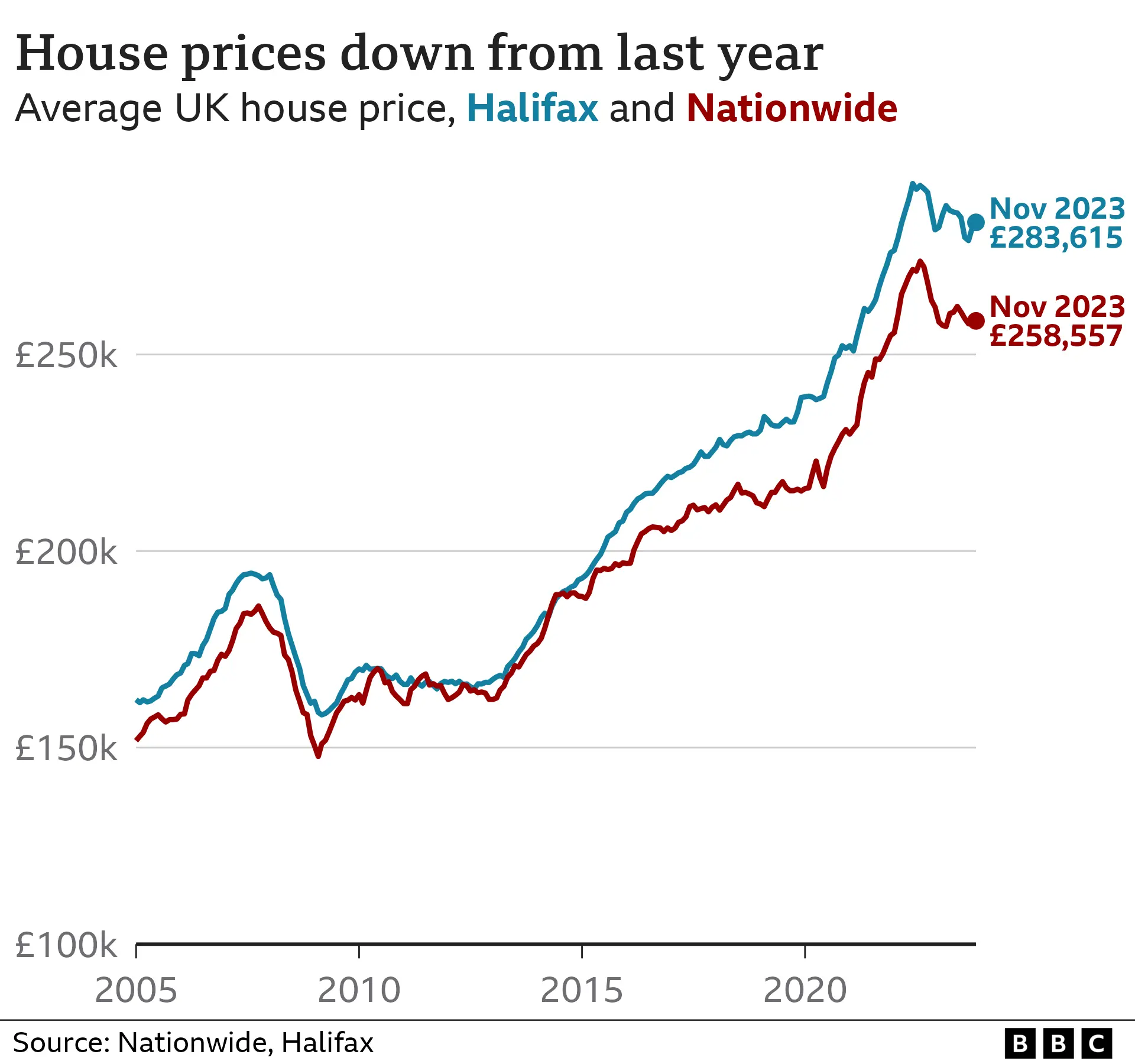

According to data from Nationwide, the typical UK house price rose to £278,880 in April, up from £277,186 in March. This represents a month-on-month increase of 0.4% and pushes annual growth to 3.0%, a notable climb from the 2.2% recorded in March.

The divergence of sentiment and asset value

A notable element of this trend is the gap between consumer sentiment and actual asset pricing. Usually, a collapse in consumer confidence serves as a leading indicator for a cooling housing market. That has not happened here, as price growth continues despite a more cautious public mood.

Robert Gardner, Nationwide’s Chief Economist, noted that the current momentum is somewhat surprising

when viewed alongside the psychological state of the British public. He pointed to the GfK headline index, which has fallen to its lowest level since late-2023, reflecting a more pessimistic outlook on personal finances and the general economy.

This pessimism is mirrored in professional sentiment. The Royal Institution of Chartered Surveyors reported a sharp decline in new buyer enquiries during March, marking the weakest reading since 2023. Despite these headwinds and the uncertainty surrounding developments in the Middle East, the market has continued to regain momentum after a slowdown at the turn of the year.

“Despite the uncertainty caused by developments in the Middle East and the subsequent rise in energy prices, the UK housing market has continued to regain momentum following the slowdown recorded around the turn of the year.” officials said

The financial buffers insulating homeowners

The resilience of the market suggests that the UK’s structural financial position is currently outweighing geopolitical shocks. This stability is likely being supported by three primary sources: debt levels, savings, and the specific mechanics of mortgage pricing.

In aggregate, household debt is currently at its lowest level relative to income seen in approximately two decades. This is bolstered by sizeable savings buffers accumulated in recent years, though Mr. Gardner cautioned that these buffers are not evenly distributed across all households. Furthermore, a period where income growth outpaced house price growth by a wide margin had already begun to improve general affordability before the current crisis.

Crucially, the cost of borrowing has not spiked in tandem with oil prices. The market relies on swap rates—the financial instruments that underpin fixed-rate mortgage pricing. These rates remain broadly in line with levels seen in late-2024 and are well below the peaks reached in 2023.

Because these swap rates have not seen a full reversal of their earlier gains, the immediate impact on monthly mortgage affordability has been limited. This creates a financial cushion that helps maintain market activity even as other sectors of the economy experience significant volatility.

Industrial costs clash with residential resilience

While homeowners remain supported by financial buffers, the broader economy is feeling the friction of the Iran war. The impact is most visible in the manufacturing sector, where the cost of raw materials, energy, and labour has surged. According to the S&P Global purchasing managers’ index (PMI), input prices have risen at one of the fastest rates since the survey’s inception in 1992, excluding the post-pandemic surge of 2022.

The disruption is physical as well as financial. Rob Dobson, director at S&P Global Market Intelligence, stated that restrictions on transit through the strait of Hormuz are causing substantial disruptions to input deliveries

, with supplier lead times stretching to their longest extent in almost four years. This has pushed business optimism in the manufacturing sector to its lowest level in a year as of April.

This results in a contrast between the manufacturing base, which is struggling with supply chain collapses and soaring energy overheads, and a housing market that continues to be driven by long-term financial buffers and stable wholesale funding rates.

The ‘E-Auto-Boom’ as a parallel adaptation

The energy shock is also triggering rapid shifts in consumer behavior, creating new pockets of growth in unexpected places. The surge in oil prices has acted as a catalyst for the electric vehicle (EV) market, as buyers pivot away from petrol to avoid volatile pump prices.

Adam Wood, managing director for Renault in the UK, described this as a seismic shift upwards

in interest. The data supports this: Renault reported that enquiries about electric vehicles on its website rose by 42%, and EVs accounted for nearly 50% of the company’s sales in April. The Renault 5 emerged as the bestselling electric car in Britain during that month.

This E-Auto-Boom

, as reported by car buying websites across Europe via The Guardian, suggests that while the Iran war is a drag on manufacturing and confidence, it is accelerating the transition to alternative energy assets. Consumers are increasingly allocating capital toward assets that provide a hedge against energy price volatility.

The risk of the worst-case scenario

The current stability of the housing market depends on one critical variable: the duration of the shock. If energy prices normalize in the coming quarters, the current softening in some sentiment indicators will likely be short-lived.

However, the monetary policy response remains a looming risk. The Bank of England held its base rate at 3.75% on Thursday, but the Monetary Policy Committee (MPC) remains alert to inflationary pressures. As reported by Yahoo Finance UK, the committee continues to monitor economic data to determine if further adjustments to the base rate are necessary to stabilize the economy.

If the MPC is forced to pivot toward aggressive rate hikes to combat the inflation driven by the Middle East conflict, the protection offered by current swap rates will evaporate. The resilience of the UK housing market has proved remarkable, but it is currently a resilience built on the hope that the geopolitical shock is a temporary spike rather than a permanent shift in the global energy regime.